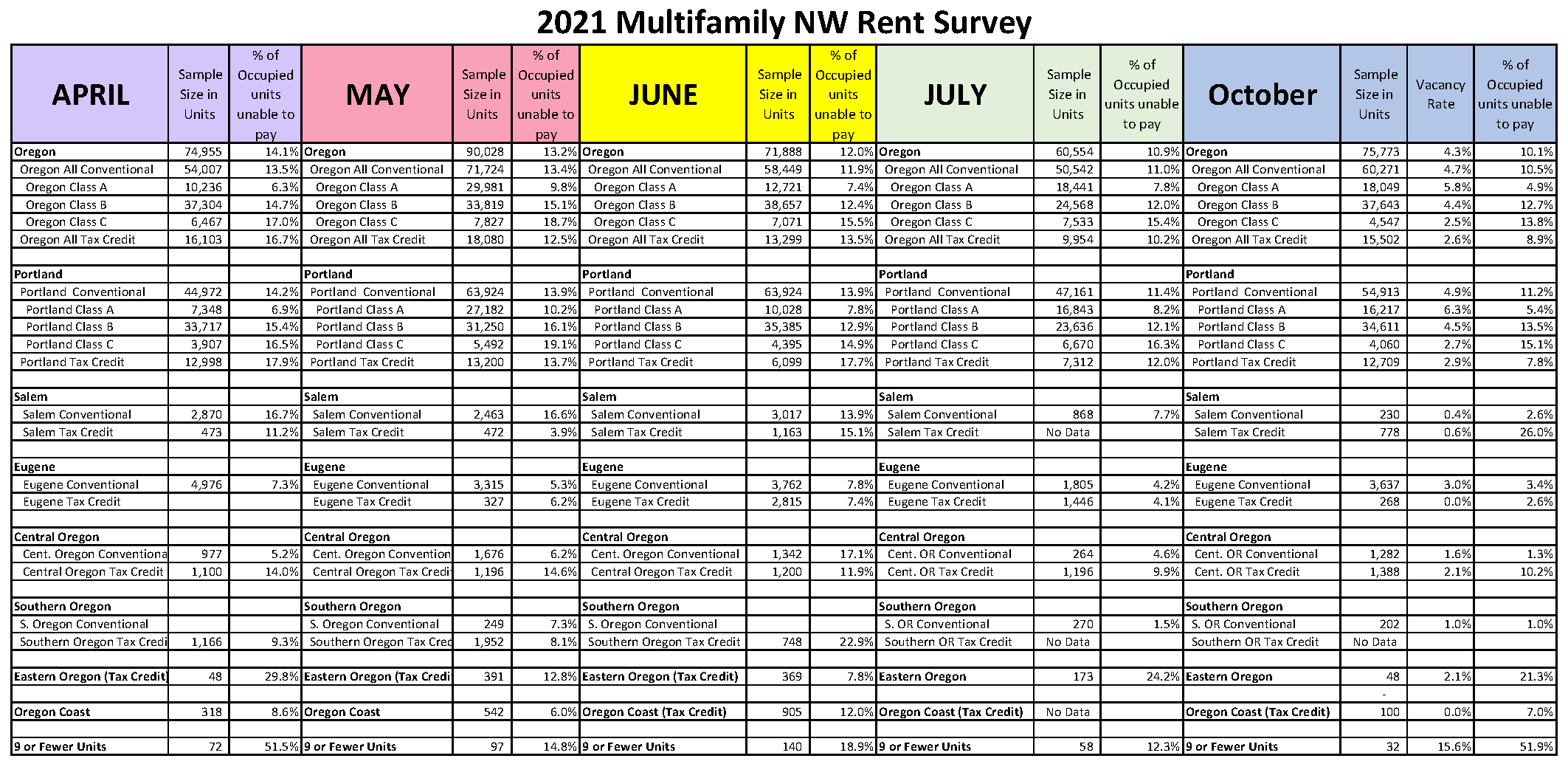

October 2021 Rent Survey Results

Click image above to view data detail

Click image above to view data detail

Multifamily NW collaborated with a broad group of housing professionals (management companies, private managers, housing authorities, nonprofits, and state agencies) to collect surveys of conventional and affordable rental housing to track trends in ability to pay rent in occupied units across Oregon.

We did not survey the months of August and September. Although this survey collects data as of the 15th, arrival of rent assistance remains unpredictable. As patterns of rent payment have been altered by Oregon legislation, tenant rent payments are continuing throughout the month, with many respondents reporting that by the end of the month payment can improve 3-5%.

Key findings for October:

- On average, 10.1% of Oregon renter households were unable to pay their rent by the 15th of the month, which represents a consistent trend in improvement since April: 1% in April, 13.2% in May, 12% in June and 10.9% in July.

- Statewide, conventional housing showed moderate improvement between July and October, improving from 11.0% to 10.5% nonpayment.

- In the statewide sample of Affordable Tax Credit units, 8.9% were unable to pay rent, a 2.3% improvement when compared to the average of 10.2% in July.

- Conventional Class-C workforce multifamily housing continued to experience the most serious housing insecurity with a 13.8% inability to pay rent. Renters in this housing type have consistently been the most impacted by inability to pay throughout the pandemic. Market rate Class C housing also reported the lowest vacancy rate of all asset types, at 2.5%.

- Data Anomalies:

- Salem Tax Credit Properties – We don’t think that non-payments are as high as 26% in the Salem area. The number of responses has varied widely for this market segment over the past three surveys, and nonpayment was tracking near the statewide average for Tax Credits in June.

- Central Oregon Tax Credits, with 1,388 units represented, have consistently reported an inability to pay of 10% or more throughout the year, while conventional units in Central Oregon have improved to 1.3%.

- Eastern Oregon had a single respondent, reporting 48 units, 1 vacant, and 10 not paying.

- Nine or Fewer Units – We only received 32 surveys from properties of 9 or fewer units. There is high variability in this cohort each month, with a different group of owners electing to respond, often BECAUSE they have non-payment. However, each month we receive consistent messages that owners of this asset class have made the decision to sell their rental units.

Additional Study Elements

- Average Arrearages: We asked respondents to provide the amount of rent owing including all current and previous months owed. 79 of respondents provided this data, representing 42,535 of the total 75,773 units in the survey. (42,535 units, 1,598 vacant, 4,414 unable to pay, for an average of 10.7% inability to pay)

|

Unit Type |

Renters Unable to Pay |

Total Owing |

Average Owed |

|

All Oregon |

4,414 |

$12,458,762 |

$2,822 |

|

Class A |

432 |

$2,103,481 |

$4,869 |

|

Class B |

3,034 |

$7,152,826 |

$2,357 |

|

Class C |

393 |

$1,392,594 |

$3,543 |

|

Tax Credit |

555 |

$1,809,860 |

$3,261 |

We calculated the average amount of total rent owed per occupied non-paying household, and sorted by unit types. On average, occupied apartments with arrearages owed $2,822.

It is interesting to compare reported arrearages from the survey to actual average payments made by the OREAP program from May 18-October 15. During this period the OERAP program had paid 14,304 households $92,371,769, for an average payment of $6,457, with an additional 24,170 households awaiting payment.

- Skips / Self-Eviction: Oregon lawmakers have expressed a concern that tenants receiving non-payment notices are "skipping" without being aware of available assistance, and consequently not appearing in county records of eviction filings. We asked respondents to indicate how many Renters in September and October skipped as a result of receiving a non-payment notice. Based on the data provided, cases of this happening are infrequent, accounting for fewer than 1/10th of 1% of the household data (.00093).

Respondent Comments

- “People are starting the assistance applications but not finishing. Many people paying after applying for assistance and then receiving large assistance checks that give more than 3 future rent payments credit on accounts and cannot get a hold of Home Forward to find out what to do with excess funds.”

- “We see that many low-income families (specially people of color) are reluctant to apply for assistance. More educational service are case management staff are needed to help these families.”

- “The majority of our past due amounts are subsidized units who have not reported any change in income… Out of the 17 tax credit units unpaid, 7 have been committed assistance through OERAP.”

- “Still haven't received the full compensation that I applied for February 2021 (Note: presumably LCF) and that the tenant applied for in summer 2021 (Note: presumably OERAP)”

- “Six of the ten residents who have not paid has applied for Renters Assistance.”

- “Ownership is not currently pursing evictions for non-payment residents.”

- “Not doing any evictions at this time.”

- “Many residents are taking advantage of the rental assistance programs. We have found many residents, carrying high delinquency balances, are fully employed, but choosing to work the system to avoid paying rent.”

- “I email out rent assistance information to anyone needing assistance and most take advantage of it. Some still don’t want help and think they can come back from this on their own.”

- “Hurry up on payment programs!”

- “Delicate process and balance once the funding applications have been made but those protections afforded applicants run out. So close yet so far, creating more stress for tenants on the brink and consternation for owners as to whether to pursue eviction or hold out for who knows how long for funding to actually arrive. Balances in the high four and five figure zone, difficult to ignore.”

- “Applications for rental assistance need to be processed in a timely fashion. The additional 20% owed to landlords from the LCF need to be paid out too (especially since they HAVE the money)!!”

Note on Methodology:

The survey asks: “How many occupied households were unable to pay full rent by the 15th day of the month?” The survey then adjusts for vacancy to arrive at the true percentage of occupied households that are unable to pay their full rent.

Definitions

Real estate professionals often use categories (A, B, or C) to describe rental properties after considering a combination of factors such as age of the property, location of the property, growth prospects, appreciation, amenities, and rental income. There is no uniform or precise formula for establishing these categories.

Class A - These properties represent the highest quality buildings in their market and area. They are generally newer properties built within the last 15 years with top amenities and demand the highest rent with little or no deferred maintenance issues.

Class B - These properties are close to Class A designation being generally older and typically offer fewer amenities. Rent is typically lower than Class A

Class C - Class C properties are typically more than 20 years old and are not as well located. Due to a variety of factors, Class C buildings tend to have the lowest rent rates in the Conventional Housing market when compared to Class A and B properties.

Conventional Housing – Market-rate housing with no household income limits, rent limits, or special programmatic requirements in the financing.

Affordable Housing – Government financed housing (Often using Tax Credits or Bonds) that impose initial household income limits and maximum rent limits, all predicated on affordability calculations based on the area median income.